The first Union Budget to shift to a debt‑to‑GDP fiscal anchor. What would this mean for capex and welfare spending, equities and rates?

Below are insights from UBS India's Chief Economist Tanvee Gupta Jain:

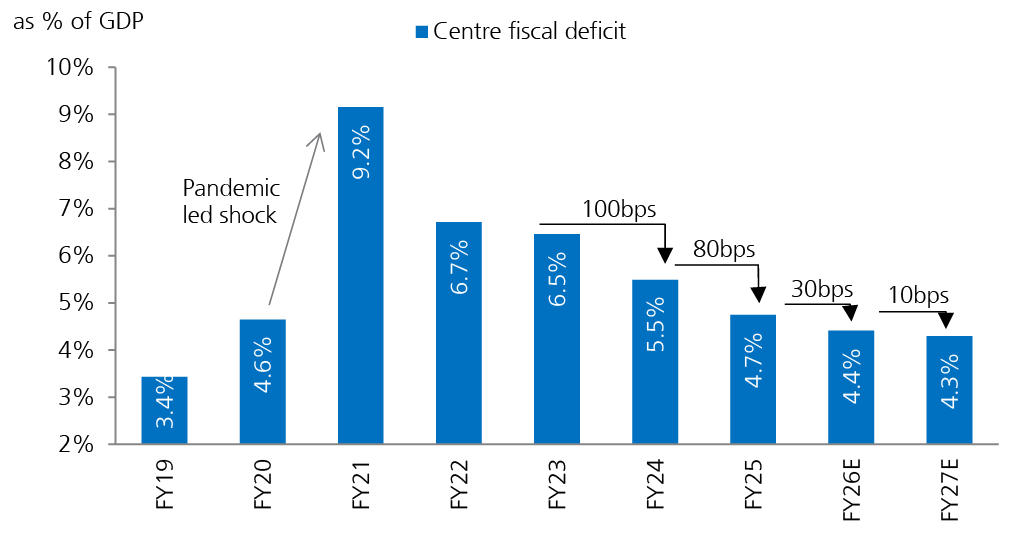

FY26 deficit on track: Fiscal buffers to help offset tax revenue shortfall

Before outlining our projections for the upcoming year, we reiterate our view that the central government will likely achieve its fiscal deficit target of 4.4% of GDP for FY26. This is despite building in a net tax revenue shortfall of Rs1.6trn (owing to the impact of the personal income tax cut, GST rate rationalisation, and slower nominal GDP growth) as well as divestment receipts falling short of budget estimates. However, we think the fiscal buffers created by: a) lower revenue expenditure (with FYTD data indicating lower spending in sectors, including water, housing and rural development, amongst others; and b) higher-than-budgeted non-tax revenues – particularly the RBI dividend transfer of an additional Rs 400-500 billion – should help partially offset the tax revenue shortfall. Media reports (link) indicate that the subsidy allocated to the Food Corporation of India (FCI) for FY26 may fall short of its projected expenditure by Rs250bn and could resort to off-budget borrowing for the first time since FY21.

FY27 Union budget to see a move towards debt-to-GDP as the fiscal metric

India's economic growth held up in FY26 despite external headwinds. The upcoming Union budget, to be announced on 1 February, is a key market event that should enable investors to understand government policy priorities, with a focus on structural reforms. Going into the next fiscal year, the government will likely move towards a new debt framework targeting its debt-to-GDP target of 50% ±1% by FY31 (from 56% estimated in FY26). This, based on our nominal GDP growth assumption of 10%YoY, will entail fiscal consolidation of 10-15bps annually. In our baseline, we estimate the central government to budget a fiscal deficit of 4.3% of GDP in FY27E. Our sensitivity analysis suggests that a 1ppt sustained increase in nominal GDP growth, say to 11% YoY during this period (versus 10% YoY growth assumed in our base case) could help in either (a) accelerating the pace of fiscal consolidation to 15-20bps annually till FY31 and/or (b) creating room for higher productive government expenditure while keeping the debt levels unchanged (Figure 5). Globally, anchoring fiscal policy to the debt-to-GDP ratio provides governments with flexibility to respond to economic shocks, while maintaining long-term sustainability. In India, we believe this could help rebuild buffers and provide policymakers with the space for growth-enhancing expenditures as and when needed.

1) Capex to stabilise; narrative on new-age technology sectors will be key

We expect central government expenditure growth of 6% YoY in FY27, based on a revenue expenditure growth assumption of 5% YoY and capex growth of around 10% YoY (vs 7% YoY estimated in FY26BE). We expect central government capex to stabilise at around 3.1% of GDP in FY27, similar to the previous year. Within capex, we anticipate a continued emphasis on infrastructure (including mobility upgrades), with a notable thrust towards defence, while maintaining stable to slightly increased allocations for roads & highways and railways. In Railways, our industrials team expects higher allocations towards rolling stock. In Defence, the team expects a pick-up in budgeted expenditure to align with strong DAC (Defence Acquisition Council) approvals over the past two years (CY2024-25 clearances of Rs 8.1 trillion, 2-3x of CY22-24). Given India’s relative under-representation in the global AI landscape, we expect the Budget to articulate a stronger AI narrative and step up funding for digital infrastructure – particularly data centres, semiconductors, electronics and R&D. Alongside AI, with the government’s ambition of achieving rare earth self-reliance, we expect the mining sector to receive incremental incentives. Many investors we spoke to expect the budget to carry forward last year’s consumption push but given the recent GST rate rationalisation (which is still unfolding) and limited fiscal space, we do not expect anything significant.

2) Higher nominal GDP growth and excise duty hike to support revenues

We expect gross tax revenue collection growth of 7% YoY in FY27E (vs 3.3% YoY recorded between April and November 2025). We believe higher nominal GDP growth will support tax revenues, even as the GST cut could weigh. Central excise collections are expected to rise in FY27 due to: a) the introduction of a new central excise duty structure on tobacco, largely cigarettes, from February 1 (new taxes are proposed in the transition from the GST compensation cess to excise duty on demerit goods), which could generate additional revenue of c0.2% of GDP; and b) we expect an excise duty hike of Rs2/litre on auto fuels including gasoline (petrol) and diesel, which could likely add 0.1% to GDP annually. We note that, for every Rs1/litre increase in excise duty on auto fuels, central government revenue could increase by about Rs160bn annually, all else equal. On the non-tax revenue front, we expect the RBI dividend to remain largely at similar levels as registered in FY26 (Rs2.7tn). We expect the government to target divestment proceeds at Rs450-500bn for FY27 (vs Rs470bn in FY26BE).

Muted impact on bond yields

10y IGB yields’ negligible reaction to RBI’s 125bps rate cuts, Rs6trn of OMO purchases, depressed CPI inflation and muted domestic demand in 2025 is, in our view, reflective of the bond market's demand-supply imbalances. In our 2026 Outlook, we noted the elongation of bond issuances’ maturity and larger SDL issuances as the real culprit here. In that context, modest fiscal consolidation is unlikely to be a market-moving event, but fiscal slippage could pressure higher. We expect 10y yields to trade in a 6.50-6.75% range in the near term, while forecasting 10y IGB to reach 6.60% by end-2026. In swaps, absent new catalysts, we think 5y OIS holds in a 5.70-5.90% range, although the front end could be volatile amidst frictional liquidity tightening into the fiscal year-end.

Equities implication

Conservative fiscal path should reassure markets on yields and equity valuations. However, the choices between higher capex vs revenue expenditure could have sectoral implications – in particular, defence capex will likely be keenly watched. While changes to personal taxation slabs are not expected, there are specific taxation actions we would watch out for: 1) the alignment of tax treatment on bank deposits vs other debt products; and 2) tweaks to securities transaction taxes. The UBS EM strategy team rates India Underweight and believes valuations remain high in the context of growth expectations for India, not meaningfully different from the rest of EM.